WHOA

Homologation Private Agreement Act

C.J. (Chris) Tijman

Without the consent of all creditors, you can still reach an agreement on a debt settlement. This has been possible since Jan. 1, 2021, with the Homologation Private Agreement Act. Does bankruptcy seem inevitable? The WHOA can offer a solution.

The WHOA stems from the initiative to adapt bankruptcy law to the requirements of our time. The WHOA is in line with a European directive to ensure that viable companies and entrepreneurs in financial difficulty have access to effective national preventive restructuring schemes that allow them to continue their activities (Directive 2019/1023 of the European Parliament and of the Council of June 20, 2019).

The purpose of the WHOA is to strengthen the reorganization capacity of companies that are in danger of bankruptcy due to excessive debt but have viable business activities. By offering a private agreement to creditors, an attempt is made to prevent an impending bankruptcy. In this way, a viable business can survive.

In addition, WHOA can be applied to wind up a company, which no longer has a chance of survival, in a controlled manner. This is done by reaching an agreement with creditors outside of bankruptcy. The advantage of this method of settlement is that a better result is generally achieved than if there were a settlement in bankruptcy.

The WHOA allows debtors to restructure debts by offering a private composition. What is extra special about this law is the fact that the agreement can also bind creditors who have not agreed to the agreement. Hence, the agreement is also called a “forced composition.”

Thus, by reaching a WHOA agreement, bankruptcy of a viable company is avoided. Moreover, the company’s board retains control of the company during the WHOA process. The board can continue to manage the company and perform legal acts. In contrast, in the case of a “regular” bankruptcy, the board’s powers are assumed by the trustee.

A WHOA agreement can change the rights of creditors and shareholders of the company. In particular, the creditors’ right to force the company to comply with the obligations incumbent on the company in the agreements entered into with them. The WHOA also allows the company to restructure ongoing agreements. This can be done by amending them or even terminating them unilaterally.

The WHOA is not intended to detract from the existing practice of out-of-court restructurings. The intention of the WHOA is to reinforce the current amicable reorganization and restructuring processes and to use the compulsory settlement under the WHOA only as a last resort

The lawyers specialized in the WHOA at Van Veen Advocaten can advise and assist you with the WHOA process. Below they explain what is involved.

Almost all types of businesses are eligible under WHOA. An exception is made for banking institutions and insurance companies. The size and legal form of the company are irrelevant. In principle, both the baker around the corner and a publicly traded company can take advantage of the possibilities offered by the WHOA.

Procedure

The WHOA process involves several steps. From drafting a starting statement, to submitting an agreement to creditors and shareholders, to voting on the agreement and homologation (approval) by the court.

Commencement of WHOA pathway

The company (or debtor) can decide on its own to initiate the WHOA process and is represented by the board. The board does not need the consent of the shareholders to do so.

The company may also choose to have a restructuring expert appointed by the court. This is an independent third party who prepares an agreement on behalf of the company and, if possible, offers it to the company’s creditors.

Not only the company can take the initiative to initiate the WHOA process, but also creditors, shareholders, the company’s works council or employee representation are authorized to do so. They will have to file a request with the court for the appointment of a restructuring expert who will go through the further process.

Closed or open

At the start of the proceedings, a choice must be made whether the proceedings will take place in private or in public. After a choice has been made, interim change is not possible.

In closed proceedings, there is no publication in the Insolvency and Commercial Register. In this case, requests are heard by the court behind closed doors and decisions are made by the court in chambers. In public proceedings, however, publication takes place in the Official Gazette, the Trade Register and the Insolvency Register. Court decisions are made in public.

The consideration to choose open or closed proceedings depends on the jurisdiction of the Dutch court, the effect of the WHOA in other European member states and the impact on security interests in the other European member states. In addition, the possible (negative) effect of publicity on the company’s operations plays a role.

Outline procedure

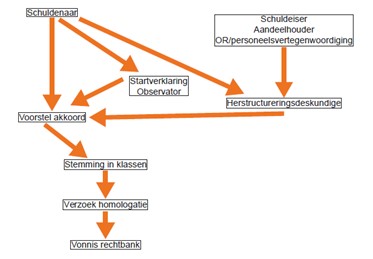

The procedure to be followed during the WHOA process to reach a binding agreement for the company’s creditors and shareholders is outlined in the flow chart below.

It follows from the diagram that the debtor can choose to offer an agreement independently or to file a so-called “starting statement” with the court. This statement shows that the company has started the WHOA process and the preparation of the agreement to be offered. The filing of the start statement gives the debtor access to various “support facilities” that can increase the chances of success of an agreement. These include, among others, the cooling-off period, lifting of attachments and suspension of bankruptcy or moratorium petitions.

Cooling off period

The company can petition the court to declare a WHOA cooling-off period. After all, it may take some time to reach a WHOA settlement. Moreover, reluctant creditors may delay or thwart this process.

During the cooling-off period, creditors cannot recover from the company’s assets unless they have been authorized to do so by the court. In addition, attachments levied against the company during the cooling-off period may be lifted by the court. Finally, requests to grant suspension of payments or declare bankruptcy of the company are suspended during the cooling-off period.

The company must file a statement with the clerk of the court at the same time as the request for the declaration of a WHOA cooling-off period, showing that the company is attempting to effect a WHOA settlement. The court will approve a request to declare a cooling-off period if such a period is necessary to allow the company to continue to operate during the preparation of the WHOA settlement and its negotiations with creditors. The court must be satisfied that the interests of the company’s joint creditors are served by the declaration of a cooling-off period. Finally, at the time the application to declare the WHOA cooling-off period is filed, the company must have already offered a composition to creditors or given an undertaking that the company will do so within a maximum of two months.

In principle, the WHOA cooling-off period lasts up to four months, but can be extended to eight months at the request of the company or the appointed restructuring expert.

Observer

At the request of the company, the restructuring expert or at the initiative of the court, an observer can be appointed by the court. If there is a cooling-off period, it is also possible for creditors and shareholders to request the court to appoint an observer.

An observer oversees the preparation of the arrangement and serves the interests of the joint creditors. In addition to the observer’s supervisory role, the observer also has an advisory role on behalf of the court.

The company or the restructuring expert will offer a WHOA agreement to the company’s creditors. With the exception of the company’s employees, the agreement may cover all types of creditors regardless of their rank and (security) rights.

It is up to the company or the restructuring expert to choose which creditors to offer the agreement to. A WHOA agreement does not have to be offered to all creditors.

If the arrangement involves different categories of creditors and shareholders, they should be placed in different classes. Creditors with the same rank and similar rights are placed in each class. For example, preferential creditors are placed in a different class than unsecured creditors or shareholders. Each class of creditors gets its own proposal.

The offer must be announced at least eight days prior to the vote.

Next, the creditors must vote on the offered settlement. Only those creditors whose rights are changed by the offered composition may vote on it. Voting is done by class of creditors. This can be done either at a physical meeting or digitally.

The agreement is adopted by the class of creditors if the creditors who voted in favor of the agreement represent at least two-thirds of the total amount of creditors’ claims within that class. The number of creditors voting for or against the composition is irrelevant.

For shareholders, the determining factor is whether the agreement is supported by a group of shareholders who together represent at least two-thirds of the total amount of issued capital belonging to the shareholders who voted within the class.

A voting record must be made of the vote. That record must be sent to those concerned within seven days.

The company must file the voting record with the homologation petition with the court. The court will set a date for hearing the homologation petition. The petition will usually be heard eight to 14 days after filing.

Prior to the hearing, creditors and shareholders may file an application for rejection of the homologation. In addition, creditors, shareholders or other third parties must notify the court in a timely manner of any reliance on a ground for rejection.

During the processing of the homologation request, the judge tests the accord. If the judge approves the agreement and thus homologates it, the agreement is binding on all creditors and shareholders involved in the agreement. This also applies to the creditors and shareholders who voted against the offered accord or abstained from voting.

When evaluating the homologation petition, the court tests whether the agreement is “pure. Is the agreement necessary? Are the formal and procedural requirements met? Is the accord feasible? And did at least one class of creditors vote in favor of the accord? The class that voted in favor of the arrangement must be a class of creditors (not shareholders) that would be expected to receive a distribution upon liquidation in bankruptcy.

In addition, the judge assesses whether the settlement is “reasonable” and does not put (classes of) creditors in a more disadvantageous position than in the case of a bankruptcy situation. The judge also assesses whether the added value of the settlement is distributed proportionately among the creditors involved.

Finally, the court will render judgment in the shortest possible time. This judgment cannot be appealed or appealed in cassation.

Different “types” of creditors may be affected by the agreement. Shareholders’ rights may also be altered. The rights of employees of the company always remain unchanged. The position of some ‘special’ creditors is considered below.

Pledge or mortgage holder

Unlike the situation where there is a corporate bankruptcy, pledge and mortgage holders may not proceed to enforce their security interests during the WHOA cooling-off period. This becomes different if the pledge or mortgage holder has obtained court authorization to do so.

In addition, a silent pledgee may not disclose the existence of a silent pledge on the company’s receivables to the company’s debtors. The pledgee also may not take payments received as a result of the established pledge. Nor may the pledgee set them off.

Suppliers

It is important for the success of the WHOA process to ensure the continuity of the company. Suppliers to the company may therefore be required to continue delivering goods ordered by the company during a declared cooling-off period. The supplier is not allowed to suspend or terminate ongoing contracts. However, the company must pay for the goods delivered during the cooling-off period within the agreed period or provide substitute security for them.

In addition, during the cooling-off period, the company may continue to use, consume and sell the goods delivered to the company by the supplier under retention of title. This is subject to the condition that this is necessary for the continuity of the business and that the interests of the supplier are sufficiently safeguarded.

Landlords

To ensure the continued existence of the business, it is often necessary for the business to be allowed to continue using the leased office or business premises.

In most cases, the rent owed to the company will be a large expense. Therefore, the company may suggest to the landlord that the lease be amended. For example, the company may try to agree on a lower rent or remove obligations included in the lease.

It is also made possible for the company during the WHOA process to terminate the lease if the landlord does not agree to the proposal made by the company. However, this is subject to the condition that the court has granted permission for the lease termination during the homologation phase. In addition, the WHOA agreement must actually be homologated.

SMEs

If creditors of the company qualify as SMEs, they are somewhat protected under the WHOA. An agreement must be offered to the class of SMEs, which states that at least 20% of their claim will be satisfied. However, the class of SMEs can agree to a lower distribution. Moreover, under circumstances, the court can determine that SMEs must settle for a lower distribution.

In principle, the company can prepare and offer an agreement to its creditors and shareholders without assistance, but it is recommended to involve a lawyer already in the preparation of the WHOA process. This is because the WHOA offers a lot of room for customization. The involvement of a lawyer is necessary when the homologation request is submitted to the court. Van Veen Advocaten can advise and support you during this part or throughout the entire WHOA process.